what is state regulated mortgage protection plan

The good news is those spammy mailers you get are also right about the price. It's usually pretty cheap to get $250k in term life insurance (assuming you're reasonably healthy).

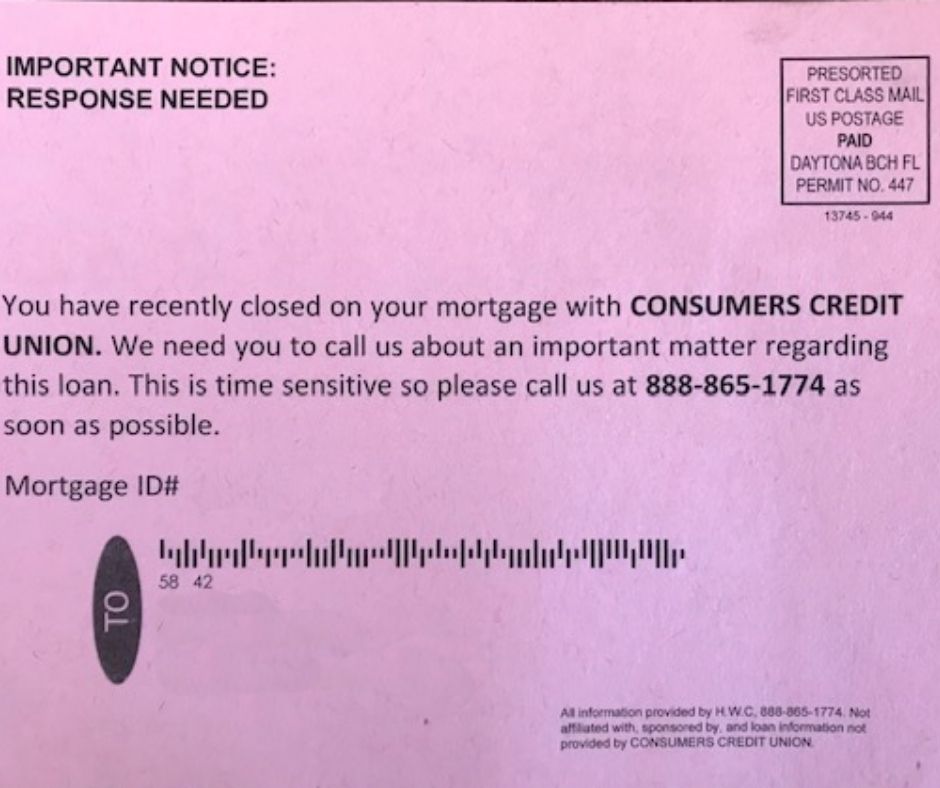

Be wary of offers asking for personal information such as social security numbers, bank account numbers, or credit card details. Most trustworthy companies will not request this data when they initially contact you to inquire if you want to buy mortgage insurance to protect you from the mortgage.